IoT connectivity resembles the final frontier for simplifying deployment of devices. Currently, the process of enabling connectivity for global devices involves needless complexity, multiple layers of lengthy administration, performance guarantees in different markets that are hard to verify, currency fluctuations and challenging-to-reach local support. Global connectivity often demands multiple vendors or even in the case of a single vendor, a service actually provided by a third party. This leaves IoT service providers facing higher costs than necessary, a convoluted management burden and the very real possibility that they can’t find out the status of their devices.

What’s needed is a simple, straightforward, fixed price service that offers assured connectivity to an agreed service level in any location with the fee based on each active device. As part of this streamlined proposition, customers – the IoT service providers – should have the ability to monitor and manage their devices and track and control costs through an easy-to-access user interface. A further benefit should be radical simplification of the onboarding process. The days of shipping plastic SIMs to factories or installing them at the point of deployment must end so logistics costs can be reduced and environmental impact minimised.

The challenge and the vision are well-understood and IoT connectivity is moving towards comprehensive communications management platforms (CMPs) that provide the visibility and control IoT service providers need. At the same time, SIM innovations in the forms of embedded SIM (eSIM) and integrated SIM (iSIM) are moving the market away from the traditional, plastic SIM and enabling SIM functionality to be integrated into IoT devices at the point of manufacture. This has the potential to put control of connectivity in the hands of IoT service providers rather than mobile operators, although both technologies can also be an opportunity for mobile operators if they see them as a means to support customers’ needs more effectively.

Management of IoT SIMs is not the same as consumer SIMs because of the sheer volume of SIMs involved and the differing requirements of use cases on the network. The range is enormous from very basic, low power, low data devices that simply ping the network to communicate that they are functioning on a sporadic basis to always-on mobile broadband devices that have mission critical functions. The communications requirements of each are completely different so there is no such thing as a one-size-fits-all IoT communications platform or network. Each use case sets its own connectivity criteria.

Platforms for growth

This need to manage IoT connectivity is being handled by CMPs which broadly originate from two types of business. One is the telecoms industry’s vendor community which has developed CMPs to support their mobile operator customers and the other is the IoT mobile virtual network operator (MVNO) sector which typically offers their own CMPs to manage the connectivity services they provide. A dwindling number of IoT service providers opt to manage IoT connectivity themselves, recognising that the burden of negotiating and managing connectivity across global markets is not a core skill and takes up significant resource and time. IoT CMPs are also a key component in the offerings from technology providers and IoT MVNOs such as 1NCE, EMnify, floLIVE, IoTM Solutions and Mavoco, says Berg Insight.

The firm has reported on third-party IoT CMP adoption, stating that 31% of the global installed base of 2.1 billion IoT SIMs were managed using third-party IoT CMPs at the end of 2021. Cisco is the largest IoT CMP provider by mobile operator partners, supporting the IoT operations of more than 60 mobile operators worldwide. The main challengers are Ericsson, floLIVE and Vodafone, which is the only mobile operator that licenses its platform to third-party service providers, and Mavoco. These companies focus on reducing the complexity associated with multinational deployments of cellular IoT devices. The China-based vendors Huawei and Whale Cloud are key players in their domestic market.

Several IoT MVNOs, including 1NCE, Eseye and Soracom, also provide white-labelled or branded IoT connectivity services via mobile operators. In addition to being a strategic partner to Deutsche Telekom, 1NCE has announced a deal with SoftBank, which will sell 1NCE’s IoT services exclusively in 19 markets across the Asia-Pacific region. IoT MVNO Aeris’ acquisition of Ericsson’s loss-making IoT Accelerator business in December 2022 marks a significant development in the CMP market. Aeris could potentially develop a managed service offering around the IoT Accelerator, which can be resold by mobile operators. The new IoT Accelerator Device Connect service already resembles the offering of many IoT MVNOs, in which enterprises can buy managed connectivity services from multiple mobile operators off-the-shelf via the Device Connect global marketplace.

New models for connectivity management

The mobile operators won’t necessarily be confined to selling their connectivity through marketplaces such as this. Many will continue to sell connectivity directly while others will utilise CMPs and MVNO providers to turn national or regional offerings into global propositions so they can retain and enlarge their business with existing enterprise customers.

The CMP market is therefore fragmented and subject to wide variance in the approaches taken by vendors to serve customers. This scale and scope is confirmed by ABI Research which has identified 62 companies offering CMPs, operated either proprietarily or commercially available to license. These companies span from connectivity resellers and aggregators to enterprise software developers, IoT service providers and carrier grade infrastructure manufacturers, the firm says.

“The largest CMP vendors such as Cisco and Ericsson, and their products have always acted as gateways for third party partnerships to jointly sell through to the same IoT enterprise customers,” explains Jamie Moss, Research Director for M2M, IoT, and IoE at ABI Research. “Today, the CMP is also a nodal product for turnkey IoT system providers, acting as a gateway product to promote the sale of value-added components of their portfolio, and ideally the full stack. From an enterprise customer perspective, CMPs are not typically charged for, but device management, and security management, and data orchestration platforms are, with CMPs acting as a single pane of glass interface over them all.”

Manage for scale – and profit

IoT connectivity is a large market and it is poised to become enormous, exacerbating the connectivity management challenges IoT service providers face and highlighting a need for automated systems that simplify both onboarding of devices and their maintenance over their lifespan. ABI Research reported at the end of 2021 that the global market for the sale of data transport, and the management of that connectivity, to original equipment manufacturers (OEMs), enterprises and municipalities was US$12.14bn. This annual total will more than double to US$31.77bn in 2026, the firm says.

“The demand-side revenue that the enterprise purchasers of these services will realise in their return on investment (ROI), be it for downstream connected services and products sold, or internal operational processes optimised will be far greater still,” adds Moss.

This is borne out by the huge predicted increased in IoT roaming traffic. Research firm Kaleido Intelligence expects IoT roaming traffic to grow from 174 petabytes in 2021 to 650 petabytes in 2026 and that’s in spite of growth being constrained due to the continuing chipset supply crisis. Overall, the firm says cellular IoT roaming connecting will exceed 850 million in 2025.

The SIM revolution

With Berg Insight now projecting that there will be 4.3 billion IoT devices connected to cellular networks worldwide by 2026 it’s clear that the days of shipping plastic SIMs to factories for installation in products are ending. Alternatives such eSIM and iSIM open up the prospect of embedding or integrating SIM functionality that can be configured for the local markets in which they are deployed remotely. This means OEMs can make a single product version, with a single stock-keeping unit (SKU) number for the global market, rather than having multiple regional versions. eSIM adoption is already well underway with familiarity driven by consumer devices and Apple’s early commitment to the technology. iSIM adoption is set to follow. However, while there are efficiencies and savings to be made by choosing eSIM and iSIM in comparison to plastic SIMs, for some customers it will still be simpler to have plastic SIMs. Typically, the cost of managing eSIMs or iSIMs and playing for remote SIM provisioning (RSP) can be greater than costs associated with traditional SIMs for use cases that involve only a few markets or even a single country. Consideration also needs to be given to the volume of devices likely to be deployed and whether they need installation and maintenance.

Lifetime favourites

It is less of a cost or barrier if a device needs to be configured at the point of deployment to have a SIM card added then than for a device that is simply mailed out to its point of use. In addition, if the device is expected to have regular maintenance this could also be an opportunity to swap the SIM at minimal additional cost. In contrast for deployment in multiple regions, at large volume and with long maintenance-free service lives, traditional SIM management activities are unviable. As the market matures, costs associated with eSIM and iSIM will reduce and fewer traditional SIMs will be utilised.

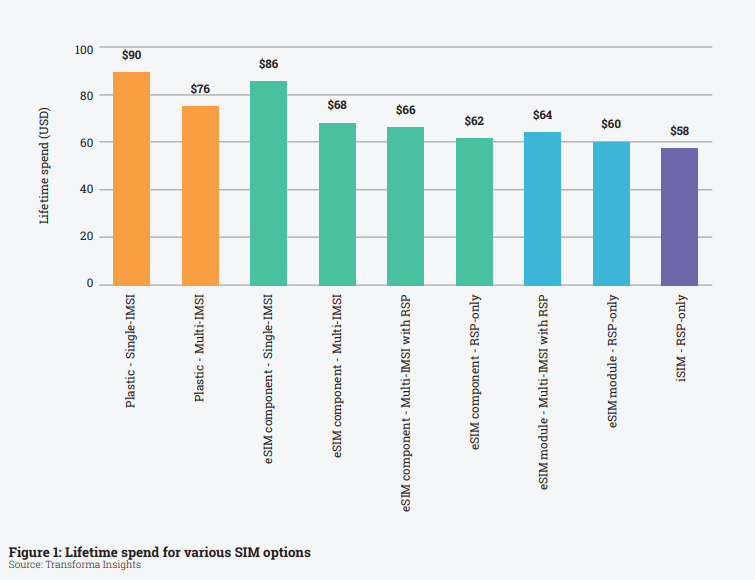

Transforma Insights has published an extensive study into the relative costs associated with eSIM and iSIM and these are set out in Figure 1, which details the lifetime spend associated with various SIM approaches. The report author Matt Hatton says: “eSIM and to a lesser extent its coming successor iSIM, have established themselves as part of the range of capabilities that need to be carefully considered by an organisation when planning a cellular-based IoT solution. Any enterprise will need to consider the overall lifetime cost of the device, with considerations of both direct and indirect costs of using the various options. In the report we examined nine costs that will determine which is the best option, including component hardware, subscription management, lifetime connectivity, logistics and compliance. All are relevant to the cost-benefit analysis of using eSIM. Overall we see there being significant savings for the average deployment from using eSIM/iSIM and RSP.”

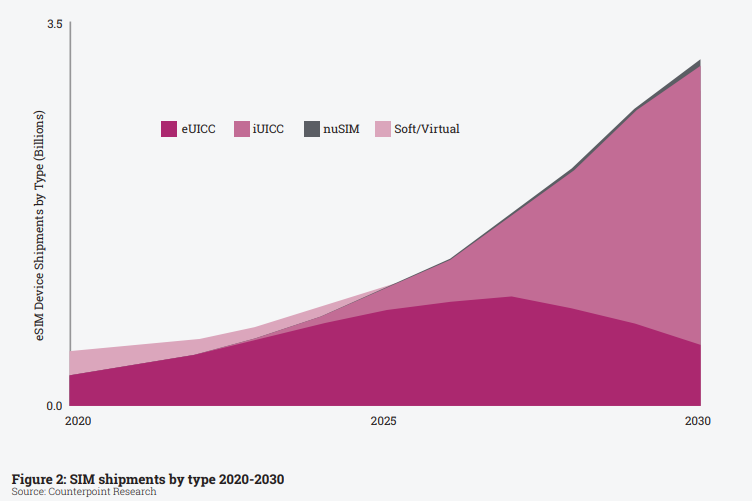

More than 14 billion eSIM devices will be shipped between 2021 and 2030, covering all form factors such as hardware-based eSIM, iSIM, nuSIM and Soft SIM, according to Counterpoint Research’s eSIM Devices Market Outlook report. eSIM uptake is poised to grow across a wide range of connected devices over the next decade, thanks to the flexibility, cost efficiency, security and other supply chain and management-related benefits offered by the embedded technology.

In 2021, more than 350 million hardware-based eSI-capable devices were shipped across a host of categories such as smartphones, smartwatches, tablets, IoT modules and connected cars. In the next five years, hardware-based eSIM will remain the dominant eSIM form factor and will account for more than half of the shipments. iSIM, which sees a SIM integrated into the chipset (SoC) offers additional benefits and shipment of these chipset began in 2022.

“The physical MFF2/WLCSP form-factor soldered eSIM (eUICC) chip has been the go-to standard for eSIM implementation even with the rise of alternative implementations such as soft SIM and nuSIM over the last decade,” says Neil Shah, the research vice president at Counterpoint Research. “However, the iSIM (iUICC) form factor will grow the fastest as the industry stakeholders move forward together to offer end-to-end support from the SIM enablement and management perspective.”

The CMP as the differentiator

That end-to-end support over the lifetime of whichever SIM form factor is selected is where the CMP providers come in again. Operators and MVNOs are certainly not excluded from this and may see their CMP as the means by which they cement customer loyalty in place of the connectivity itself. The promise of eSIM and iSIM is greater flexibility and the choice to switch operators to better coverage or a better deal. This presents both a threat and an opportunity for a mobile operator.

On one hand, they can more easily lose customers and face weakened ability to lock customers into their propositions for the long-term. On the other hand, they have the opportunity to add value by offering high-quality, ubiquitous coverage over multiple operators’ networks. It may turn out that the CMP is the critical differentiator. IoT service providers will utilise CMPs that present device information in the way they prefer and enable them to manage their device estate in simple ways that don’t require them to become telecoms experts.

Ultimately, it might be moving CMP that becomes the bigger barrier and moving operator just something that seamlessly happens as IoT connectivity is optimised automatically for every device. With a deployed base of millions for a growing number of deployments, it’s easy to see how customer loyalty shifts from the connectivity provider to the CMP provider. That doesn’t exclude operators but it does mean they need to offer CMPs with the features, capabilities and business models what IoT service providers want to engage with.

Comment on this article below or via X: @IoTNow_OR @jcIoTnow