Transforma Insights analysts have been forecasting the Internet of Things market opportunity for over a decade. Back in 2011 our analysts’ expectation of 12 billion IoT devices by 2020 was close to the bottom of the league table of predictions but proved to be easily the most accurate. Today, as Transforma Insights, our team continues to provide the most extensive and deeply researched forecasts of the IoT, making ours the benchmark against which all predictions of IoT market growth should be compared. In this article article, Matt Hatton, the founding partner of the firm, presents the key findings of its latest annual analysis.

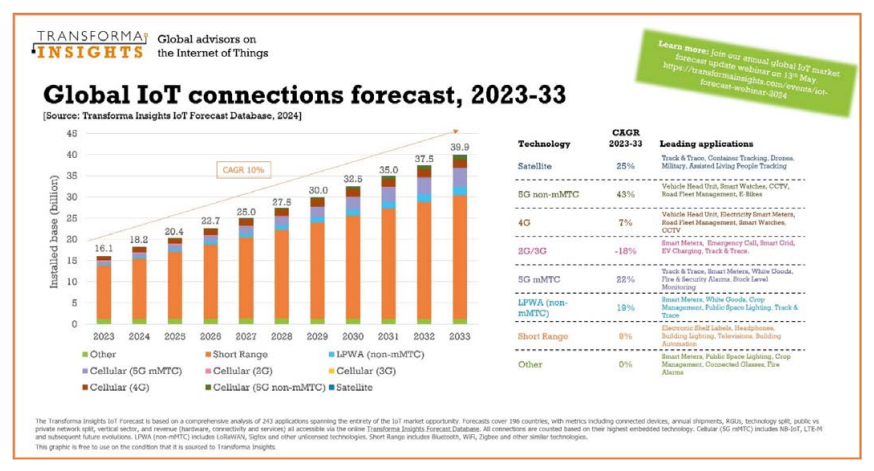

At the end of 2023 there were 16.1 billion active IoT devices, a figure which will grow to 39.9 billion in 2033, at a compound annual growth rate (CAGR) of 10%. In 2033 the consumer sector will account for 61% of all connections. Of the enterprise segment in 2033, 35% of devices will be accounted for by ‘cross-vertical’ use cases such as generic track-and-trace, office equipment and fleet vehicles, 24% by utilities, most prominently smart meters, 22% by retail/wholesale (predominantly payment processing devices and electronic shelf labels), 7% by government, 4% by transport and logistics, and 3% for agriculture. The single biggest use case is Consumer Internet & Media devices, accounting for 32% of all devices in 2033. The next largest is smart grid, including smart meters, representing 11% of connections.

The main thing to note is that there is no ‘hockey stick’. There are sometimes a few fast growing markets, for instance the requirement for all cars in Spain to be equipped with a connected beacon will trigger very rapid adoption over a short period of time. But that is the exception rather than the rule, and the diversity of IoT means that such rapid growth markets are counterbalanced by those with longer time horizons. Furthermore, inertia in many markets and the dependency on user replacement rates (such as buying new cars) also act to maintain a steady linear growth.

Connectivity technologies in transition

Short range technologies will dominate connections, growing from 12.6 billion in 2023 (accounting for 79% of connections) to 29.3 billion (73%) in 2033. This reflects the fact that most IoT devices are consumer electronics and are deployed indoors, and thus typically have ready access to a private (usually Wi-Fi) network.

Cellular connections will grow from 1.9 billion at end 2023 to 7.5 billion at end 2033. A lot of Transforma Insights’ focus is on wide area connectivity, and it is interesting to track the trajectory of the various generations of cellular technologies.

In total, 5G will grow from 650 million to 5.5 billion connections over the forecast period. The majority, 4.4 billion, will be using massive machine type communications (mMTC) technologies, predominantly comprising NB-IoT and LTE-M, both of which are nominally 5G technologies and are future-proofed to be supported on 5G core networks. Today China strongly dominates the 5G mMTC market due to extensive NB-IoT deployments. It accounted for 73% of the deployed base at the end of 2023, although by 2033 its global share will fall to 43%. The biggest use cases will be Track & Trace, smart meters and white goods. By 2033 there will be 1.1 billion ‘full’ 5G New Radio, or ‘non-mMTC’, devices up from 30 million today. The biggest 5G non-mMTC use case is vehicle head units, accounting for 41% of connections in 2033.

The use of 4G will peak in 2032 at 1.9 billion connections, after which we expect it to decline. 2G and 3G will gradually be phased out over the forecast period too. By 2029 we anticipate no shipments of devices where 3G is the highest technology, and 2G shipments will be just over 100,000.

As well as cellular-based low power wide area (LPWA), i.e. the 5G mMTC described earlier, we also track unlicensed technologies such as LoRaWAN and Sigfox in our ‘LPWA non-mMTC’ category. These will grow from 361 million connections in 2023 to over two billion connections in 2033. The combination of the two categories of LPWA, both mMTC and non-mMTC, will amount to 6.5 billion devices in 2033, or 22% of all IoT devices, up from 8% today.

We should note that the generation splits as described above relate to the highest embedded technology.

Almost a trillion dollar market by 2033

In revenue terms, the total IoT market (defined as including connectivity modules, value added connectivity, and core associated applications) in 2023 was worth US$335 billion, a figure which will rise to US$934 billion in 2033. Value added connectivity will account for 10% of spend in 2033, with the connectivity modules accounting for a further 4%. The remainder is accounted for by what we term ‘Service Wrap’, i.e. the value of the IoT application that rides on top of the connection, such as fleet management or a security alarm service.

In financial terms, the biggest vertical sector is consumer, generating US$290 billion in revenue in 2033, or 31% of the total market value. Cross-vertical applications account for 22%. The remaining 47% is sector-specific applications across sectors such as energy, transport, retail and healthcare.

Geographically, China, North America and Europe dominate, accounting for 32%, 21% and 19% respectively of the total value of the IoT market in 2033.

Comment on this article via X: @IoTNow_ and visit our homepage IoT Now